Table of Contents

For those over 55 with a mortgage-free property or a small remaining mortgage, now might be the perfect time to secure your financial future. Reverse mortgages in Canada, such as the CHIP mortgage, are popular solutions for seniors looking to access equity in their homes.

Today’s economy makes managing money challenging. This is especially true for seniors on fixed incomes. Yet, securing your future is quite possible with the right financial tools. Here’s more about reverse mortgages in Canada and how they can benefit you or your loved ones.

What is a Reverse Mortgage in Canada?

A reverse mortgage is a loan secured against your home. It lets you turn your home equity into tax-free cash without selling. If you’re 55 or older, you are eligible for this program. Here are some key features of reverse mortgages in Canada:

- No Monthly Mortgage Payments. As long as you or your spouse live in your home, you will never be required to make a mortgage payment. The loan is repaid when you sell your home, move out, or pass away.

- Tax-Free Income. The money you receive from the reverse mortgage is not added to your taxable income. It won’t affect your Guaranteed Income Supplement or Old Age Security. It also won’t affect any other benefits you receive.

- Flexible Use of Funds. There are no restrictions on how you use the money from your loan. You can use it to pay off debt, cover medical expenses, fund home renovations, or enjoy your retirement.

- Retain Home Ownership. You don’t give up ownership or control of your home. You can continue to live in your home for as long as you wish.

- Home Equity Growth. Your home equity continues to grow with your property’s appreciation in value. Even with a growing mortgage balance, your equity can increase over time.

- Non-Demand Loan. Unlike most mortgages, a reverse mortgage isn’t a demand loan. This means that even if your property’s value decreases, the bank cannot foreclose on the mortgage.

Addressing Concerns About Leaving Money to Family

Many people worry about obtaining a reverse mortgage. They fear that they will leave no equity for their family after they die. However, even with modest real estate value growth, this is unlikely to be an issue.

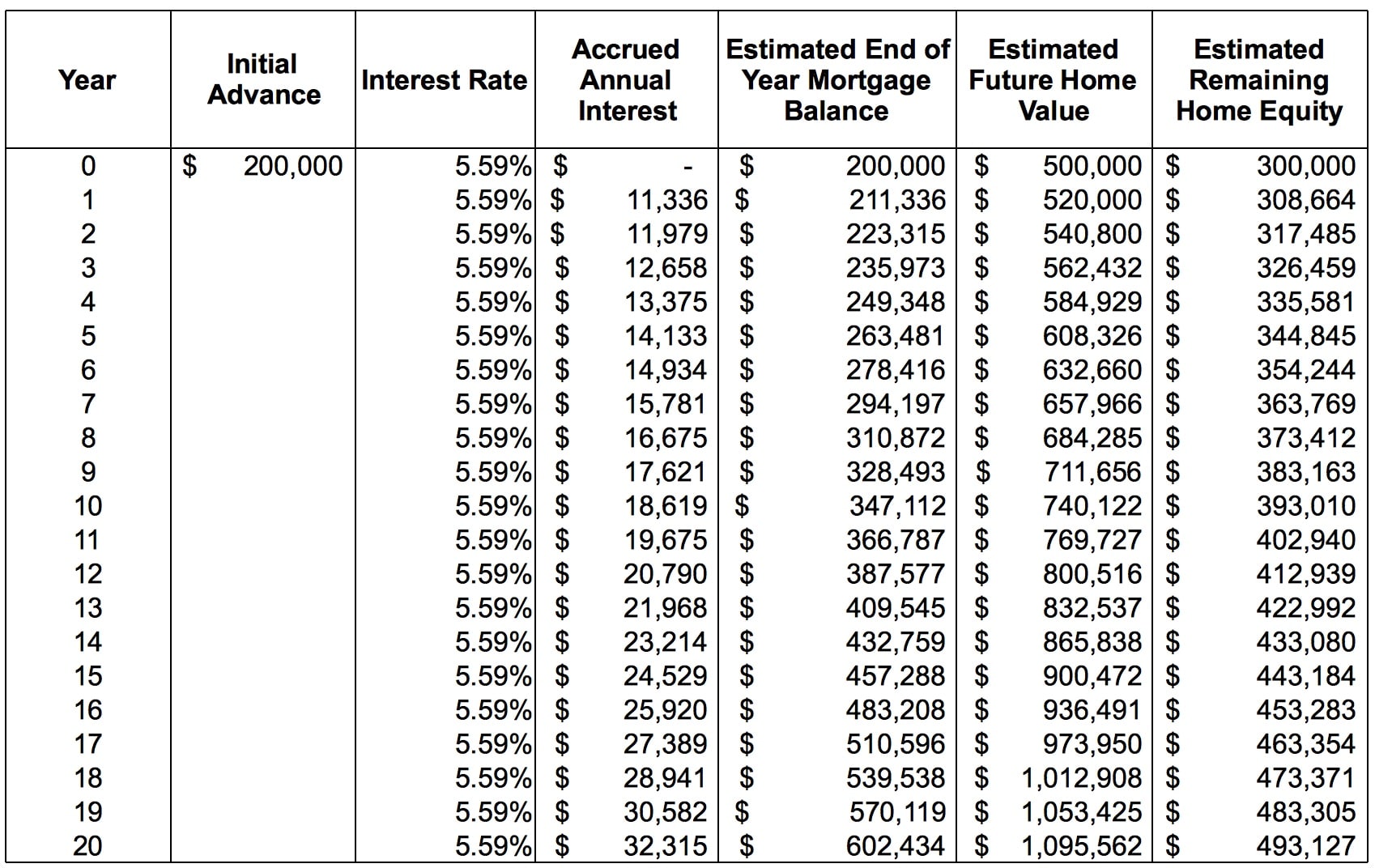

For example, consider a $200,000 mortgage on a $500,000 home. It has 4% average appreciation and a 5.59% interest rate. Over 20 years, the equity increases from $300,000 to $493,000. Despite the growing principal balance, the property equity still grows.

Furthermore, you’ve worked hard to build up equity in your home. If you need to access some of it to enjoy your retirement, you shouldn’t feel bad about using it. Your family likely wants you to be comfortable and enjoy your life. Reverse mortgages in Canada can offer both money and peace of mind.

Understanding the Interest Rates

Some seniors worry about the interest rates on reverse mortgages. They worry when they compare them to traditional mortgage rates. In an era of 2.49% interest rates, a 5% rate might seem high. But there are reasons for this.

- Risk and Return. Higher-risk investments require higher returns. While a reverse mortgage may not seem risky for a lender, it is riskier compared to other financial products.

- Benefits Provided. The higher interest rate compensates for the benefits of the CHIP reverse mortgage. These benefits include the non-demand nature of the loan and the flexibility it provides.

- No Credit or Income Requirements. Reverse mortgages are unlike traditional mortgages. They have no credit score or income requirements.

- Low Penalties. It also has flexible rules for death or moving to a care facility. They ensure that no surprise issues could cause a large mortgage penalty.

- Power of Attorney. Reverse mortgage lenders allow for a Power of Attorney to sign for the homeowner. This adds an extra layer of convenience.

Alternative Mortgages

I believe that reverse mortgages in Canada are viable and legitimate products. They are sometimes confused with their US counterparts. I have heard of issues with reverse mortgages in the US. Yet, as great as they are, they are not always the right product for everyone over the age of 55.

Thankfully, depending on your circumstances, we have many other products available. For example, we can structure a home equity line of credit (HELOC) to work in a similar manner.

A Real-Life Example of a Reverse Mortgage

I once spoke with a friend. He wanted to buy a home in a good area, but couldn’t afford it without selling his current home. He considered moving to a less expensive area, but was unhappy with the idea.

I suggested he consider a reverse mortgage. It could provide the funds to buy the home he wanted in his preferred area. Unfortunately, he dismissed the idea, concerned about losing equity. In the end, he moved to a less desirable area and missed out on greater property appreciation and a more enjoyable lifestyle.

Conclusion

If you are over 55, and want to secure your financial future with a reverse mortgage in Canada, give me a call. We can discuss your options and determine if a reverse mortgage is the right solution for you. If it isn’t, I can provide other mortgage options that suit your needs. Contact me today to get started on your journey to financial stability and peace of mind.